Tag: metric

-

Keeping a King in the Castle with a Well-maintained Cash Reserve

You’ve no doubt heard the old business cliché “cash is king.” And it’s true: A company in a strong cash position stands a much better chance of obtaining the financing it needs, attracting outside investors or simply executing its own strategic plans. One way to ensure that there’s always a king in the castle, so…

-

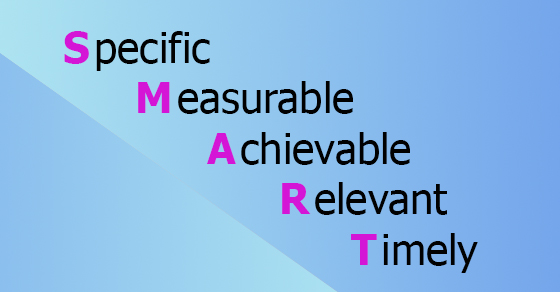

Get SMART When Setting Strategic Goals

Strategic planning is key to ensuring every company’s long-term viability, and goal setting is an indispensable step toward fulfilling those plans. Unfortunately, businesses often don’t accomplish their overall strategic plans because they’re unable to fully reach the various goals necessary to get there. If this scenario sounds all too familiar, trace your goals back to…

-

A Midyear Review Should Go Beyond Financials

Every year is a journey for a business. You begin with a set of objectives for the months ahead, probably encounter a few bumps along the way, and reach your destination with some success and a few lessons learned. The middle of the year is the perfect time to stop for a breather. A midyear…

-

Could Your Next Business Loan Get “Ratio’d?”

We live and work in an era of big data. Banks are active participants, keeping a keen eye on metrics that help them accurately estimate risk of default. As you look for a loan, try to find out how each bank will evaluate your default probability. Many do so using spreadsheets that track multiple financial…