Tag: 401(k)

-

New Law Provides a Variety of Tax Breaks to Businesses and Employers

While you were celebrating the holidays, you may not have noticed that Congress passed a law with a grab bag of provisions that provide tax relief to businesses and employers. The “Further Consolidated Appropriations Act, 2020” was signed into law on December 20, 2019. It makes many changes to the tax code, including an extension…

-

Using Your 401(k) Plan to Save This Year and Next

You can reduce taxes and save for retirement by contributing to a tax-advantaged retirement plan. If your employer offers a 401(k) or Roth 401(k) plan, contributing to it is a tax-wise way to build a nest egg. If you’re not already contributing the maximum allowed, consider increasing your contribution rate between now and year end.…

-

Are Your Employees Ignoring Their 401(k)s?

For many businesses, offering employees a 401(k) plan is no longer an option — it’s a competitive necessity. But employees often grow so accustomed to having a 401(k) that they don’t pay much attention to it. It’s in your best interest as a business owner to buck this trend. Keeping your employees engaged with their…

-

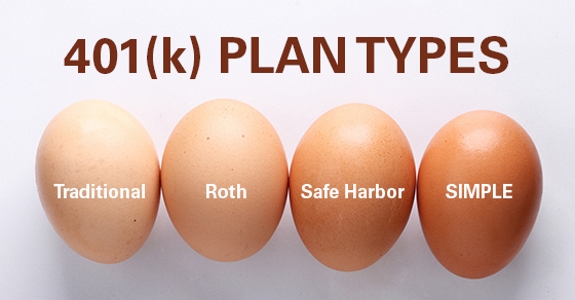

Finding a 401(k) that’s Right for Your Business

By and large, today’s employees expect employers to offer a tax-advantaged retirement plan. A 401(k) is an obvious choice to consider, but you may not be aware that there are a variety of types to choose from. Let’s check out some of the most popular options: Traditional. Employees contribute on a pre-tax basis, with the…